Originally posted in Financial Advisor (fa-mag.com) on July 1, 2019

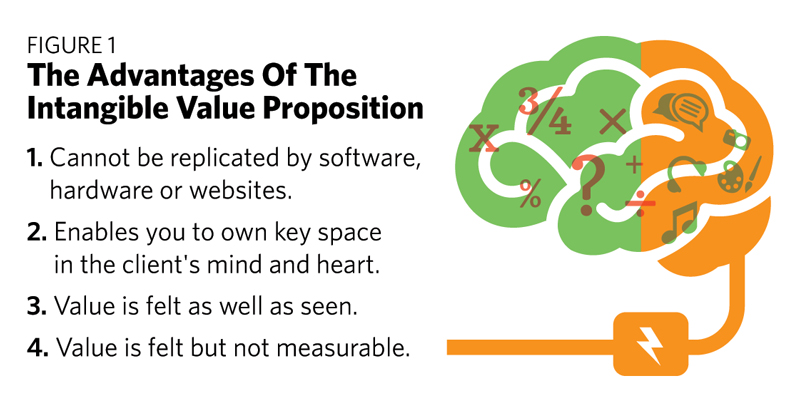

In my last column, I described how messy a financial advisor’s value proposition is when it’s based on a return on investment and how unsustainable that value offering really is. Trying to guess the future and constantly outperform the market is an activity done out of hubris. Your offering, to be truly valuable, must be sustainable and immune from techno-threats that continue to threaten you with obsolescence. Author Daniel Pink said the value propositions of the future need to be clearly housed in the right side of the brain. (See Figure 1).

What does this mean? The following graphic might help as it illustrates four ways that advisors can differentiate themselves.

If software, hardware or websites are available to do what you do, you’re in trouble. If clients can compare what you do to what most other advisors do, you’re in deeper trouble. If your firm’s history is a story of numbers, not the story behind the numbers, your relationships will inevitably be at risk.

The more important message coming from your business to your clients today needs to be a message of what you are going to do to help them accomplish the best life possible with the money they have. (I call this “Return on Life,” or “ROL,” as a counterpoint to “ROI.”) If this is not your message, then you are on shaky ground, because it’s simply unsustainable to try to outdo everyone else at gathering and managing money.

The three primary objectives in a greater ROL are to:

1. Help bring clarity to your clients about the purpose of their money.

2. Help your clients understand the personal side of planning. Numbers tell us nothing if we don’t know the story behind them.

3. Help clients answer the three big money/life questions.

First Objective: Clarity About Money’s Purpose

There is a point to having money. There is a purpose for gathering wealth. Too often, wealth managers focus on growing the tree instead of harvesting and building with the timber. Yet the conversation about money’s purpose is grossly neglected in the average planning dialogue. “What is the money for?” may be the simplest and most necessary question you ask.

To help your clients with this discussion, you need to put forth a point of view on what the money is all about. Wear the philosopher’s hat and explain that you understand the bigger picture, the more meaningful aspect, what matters most—that there is meaning attached to their means and that there is purpose attached to their purse.

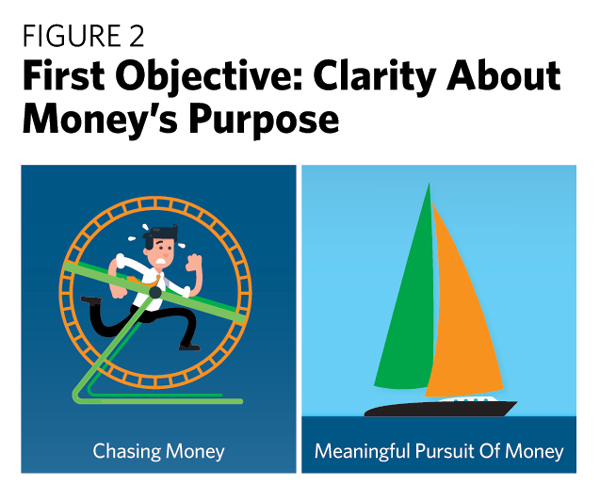

The Figure 2 graphic has proved to be a great stimulus to such a conversation, helping life-centered planners explain the difference between chasing money and pursuing a meaningful objective with it.

Everyone knows people who feel like the gerbil in the wheel when they are just chasing money, not knowing what will happen if they ever catch it. The sail represents a different philosophy: Money is nothing more than something we use to navigate. It is not the shore we sail for, the water we sail upon, or even the vessel that transports us and our loved ones. It’s just a utility. Yet it must be managed skillfully if we hope to arrive safely.

Second Objective: The Story Behind The Numbers

Advisors who rethink their value in these terms must also master the art of learning their clients’ stories. That will not only help us make a personal connection, but lead us to planning that’s more precise.

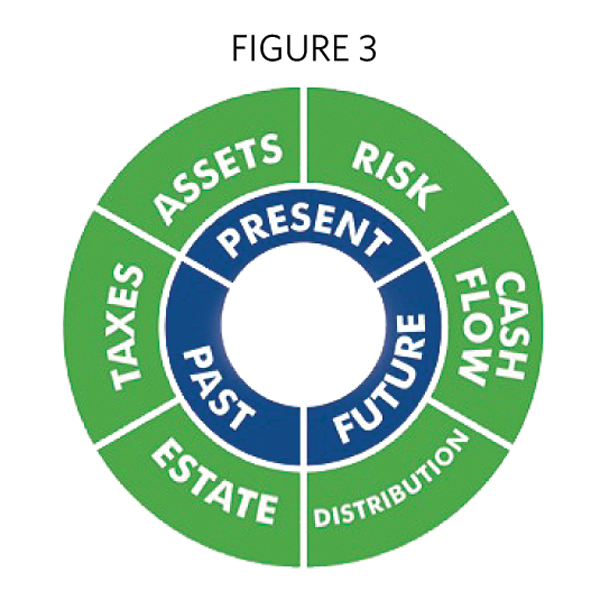

Graphics like the one in Figure 3 illustrate for the client that your process isn’t one-size-fits-all—that it’s deeply personalized. The outer circle represents what we might call “money mechanics” or the necessary focuses of a financial planning process. Many of those functions can be replicated by technology and imitated by poseurs in planning. Once we are on the same page with the client that the primary objective is a greater “return on life,” then the work comes to be about personal discovery—not just of their assets but of their story: past, present and future.

Shakespeare wrote in The Tempest, “What’s past is prologue.” We need to know of our clients’ experiences with money, because contained in those experiences are the blueprints for their financial status and potential future. We also need to understand clients’ experiences with other financial professionals, good or bad, as those too have a bearing on the risks they will or will not be willing to take.

If your primary goal is to build a lasting relationship, then it’s not a good idea to be collecting numbers and facts before you’ve gathered a client’s personal story. And that story can be gleaned by asking the three big money/life questions.

Third Objective: The Big Money/Life Questions

At ROLAdvisor.com, we have developed a digital discovery process to help clients answer these three questions. We have a “Fiscalosophy” profile designed to discover their specific financial philosophy on key money issues such as managing debt, investing, saving, retiring, supporting children and managing risk.

To better understand the present, we administer the “ROLIndex”—a reflective exercise for clients to rate the level of satisfaction they are deriving from the application of their money into 10 aspects of life: work, residence, leisure, health, relationships, achievement, learning, purpose, security and autonomy. This exercise gives clients a highly personalized portrait of their progress with money, as well as an actual number for how they rate their “return on life” at present. This places the emphasis not on how they’re doing against the markets, but instead on how they’re doing against their potential.

Their story is ongoing. But the future will be determined by the transitions the clients are facing now. Money goes into motion when life goes into transition, so it is imperative that life-centered planners understand exactly the transitions their clients are facing. There is no better track for pertinent planning and relationship-building than helping clients financially navigate every meaningful transition in their life.

This means advisors need a more sustainable value offering. For that, I’ll close with a fitting acronym: AUM.

• Align your client’s means with their meaning.

• Understand their unique story.

• Monitor their life’s transitions.

Thinking about your clients—not their assets—is the more important factor you can focus on. Once you get it right, no client will entertain going elsewhere or question what he or she is paying for. People know innately when they are being served properly.

Mitch Anthony is the creator of Life-Centered Planning, the author of 12 books for advisors, and the co-founder of ROLadvisor.com and LifeCenteredPlanners.com.